Project Accounting: Complete Guide for Businesses (2026)

Manage your project finances with confidence using this complete project accounting guide covering processes, best practices, software, and cost control.

Managing multiple projects without clear visibility into costs, budgets, and profitability can quickly lead to overspending, billing errors, and reduced margins. When financial information is scattered across spreadsheets and disconnected tools, making timely decisions becomes difficult. Project accounting helps you track project-specific finances, monitor costs in real time, and maintain better control over every stage of a project's lifecycle.

This guide explains how project accounting works, why it matters, the key processes and methods involved, common challenges, and practical best practices. You'll also discover how the right software can simplify financial management and improve project profitability.

What Is Project Accounting?

Project accounting is a financial management approach that records, monitors, and analyzes the income, expenses, budgets, and resources associated with individual projects. It gives a clear view of each project’s financial performance, helping you control costs, improve profitability, and make informed decisions throughout the project lifecycle.

Why Project Accounting is Important

Managing project finances effectively is essential for keeping budgets under control and ensuring every project contributes to business growth. Project accounting provides detailed financial insights at the project level, helping you make timely decisions, improve efficiency, and maximize profitability.

- Improves Project Profitability: Tracks the financial performance of each project separately, making it easier to identify profitable projects and address those that are exceeding budgets.

- Provides Better Cost Visibility: Monitors project expenses as they occur, helping teams detect unexpected costs early and take corrective action before they impact the budget.

- Supports Smarter Resource Planning: Shows where labor, equipment, and other resources are being used, allowing you to allocate them more efficiently across projects.

- Enables More Accurate Project Estimates: Uses historical project cost and performance data to create realistic budgets and pricing for future projects.

- Strengthens Client Billing and Financial Transparency: Maintains detailed records of project costs, billable hours, and milestones, making invoices more accurate and building greater trust with clients.

Did you Know?

According to the Project Management Institute’s Project Success Report, only 48% of projects are considered successful, while 40% achieve only partial success and 12% fail. Highlighting strong financial planning, accurate cost tracking, and timely reporting plays a critical role in improving project outcomes.

Project Accounting vs Financial Accounting: Key Differences

Although both project accounting and financial accounting help you manage finances, they serve different purposes. Project accounting focuses on the financial performance of individual projects, while financial accounting provides an overall view of the organization’s financial health. Understanding these differences helps you choose the right approach for managing projects and making strategic financial decisions.

| Aspect | Project Accounting | Financial Accounting |

|---|---|---|

| Primary Focus | Tracks the financial performance of individual projects. | Tracks the overall financial performance of the entire business. |

| Scope | Covers project-specific budgets, costs, revenue, and profitability. | Covers all business transactions, assets, liabilities, revenue, and expenses. |

| Timeframe | Follows the lifecycle of each project, regardless of accounting periods. | Reports financial results for fixed periods such as monthly, quarterly, or annually. |

| Cost Tracking | Monitors project expenses, labor costs, materials, and billable hours in detail. | Records overall business expenses without separating them by project. |

| Decision-Making | Helps project managers control budgets, allocate resources, and improve project outcomes. | Helps business leaders evaluate company performance and make financial decisions. |

| Reporting | Generates project-level reports, including cost, budget, and profitability analysis. | Produces financial statements such as the balance sheet, income statement, and cash flow statement. |

| Primary Users | Project managers, operations teams, finance teams, and department heads. | Executives, investors, auditors, regulatory authorities, and finance departments. |

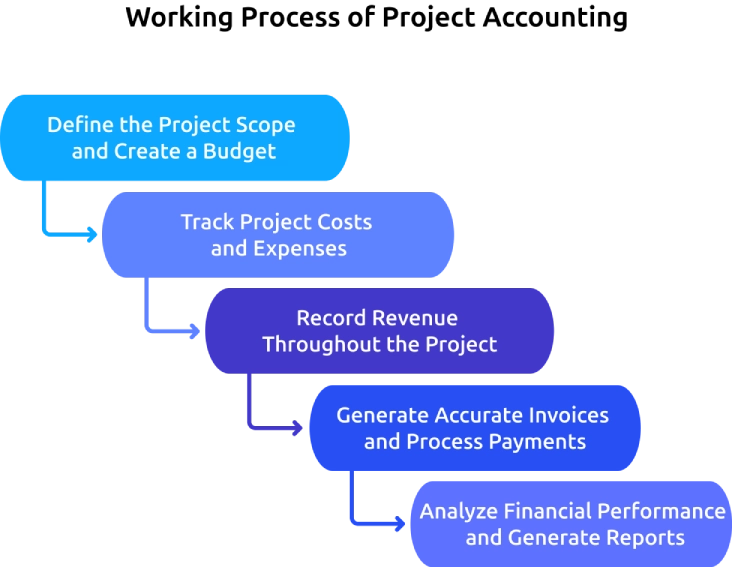

How Does the Project Accounting Process Work

A structured project accounting process helps you monitor finances from the beginning of a project until its completion. Each stage focuses on controlling costs, tracking progress, and measuring profitability, ensuring projects stay financially healthy and aligned with business goals.

1. Define the Project Scope and Create a Budget

The process begins by outlining the project’s objectives, timeline, deliverables, and available resources. Based on these details, you can estimate labor, material, equipment, and operational costs to create a realistic budget that serves as the financial benchmark throughout the project.

2. Track Project Costs and Expenses

As work progresses, every project-related expense is recorded, including employee hours, material purchases, contractor payments, travel costs, and other operational expenses. Tracking these costs in real time helps you identify budget variances early and take corrective action before overspending affects project profitability.

3. Record Revenue Throughout the Project

Revenue is recognized according to the project’s billing model and accounting standards. Whether payments are tied to project milestones, completed work, or time and materials, recording revenue accurately provides a clear picture of the project's financial performance at every stage.

4. Generate Accurate Invoices and Process Payments

Once billable work is completed, create invoices based on approved hours, project milestones, contracts, or recorded expenses. Accurate billing minimizes disputes, speeds up payments, and helps maintain healthy cash flow throughout the project lifecycle.

5. Analyze Financial Performance and Generate Reports

After recording project costs and revenue, compare actual spending against the planned budget to evaluate financial performance. Detailed reports on profitability, budget utilization, resource costs, and revenue help you identify improvement opportunities, make informed decisions, and plan future projects more effectively.

What are the Most Common Project Accounting Methods

Choosing the right project accounting method helps you recognize revenue accurately, manage cash flow, and comply with accounting standards. The best method depends on factors such as project duration, contract type, payment structure, and how project progress is measured.

Percentage of Completion

This method recognizes revenue and expenses gradually as the project progresses.

How It Works: You can determine the portion of work completed using factors like costs incurred, labor hours, or achieved milestones, and then record revenue in proportion to that progress.

Best For: Long-term projects such as construction, engineering, infrastructure, and large consulting engagements where work spans several months or years.

Milestone Billing

This is a project accounting method where revenue is recognized at specific stages of project completion.

How It Works: Revenue is recorded, and invoices are generated when predefined project milestones are completed. Each milestone marks a key stage of the project, ensuring payments are tied to progress.

Best For: Software development, marketing agencies, consulting firms, product development, and projects with clearly defined deliverables.

Completed Contract Method

This method is an accounting approach where revenue and expenses are recognized only after a project is fully completed.

How It Works: You may defer recording all project-related revenue and costs until the project is finished and all contractual obligations are met. Once completed, the total revenue and expenses are recorded at once, providing a clear final financial outcome without tracking progress during the project.

Best For: Short-duration projects, fixed-price contracts, and projects where the final outcome or total costs cannot be measured reliably until completion.

Key Benefits of Project Accounting

Keeping project finances organized is about more than tracking numbers, it helps you make confident decisions throughout the project lifecycle. With the right project accounting approach, you can monitor financial performance, control spending, and improve the success of every project.

- Gain Clear Visibility into Project Profitability: Track each project's revenue, expenses, and margins to identify which projects generate the highest returns and which need immediate attention.

- Stay Ahead of Budget Overruns: Monitor project costs in real time so you can spot unexpected expenses early, adjust spending, and keep projects within budget.

- Make Better Use of Time and Resources: Understand how labor, equipment, and other resources are being utilized across projects, helping you reduce waste and improve overall efficiency.

- Plan Future Projects with Greater Accuracy: Use financial insights and historical project data to create realistic budgets, timelines, and cost estimates for upcoming projects.

- Build Trust Through Accurate Billing: Generate invoices based on actual project progress, approved work, and recorded expenses, giving clients greater transparency and reducing billing disputes.

- Make Faster, More Informed Decisions: Access project-level financial reports that help you evaluate performance, identify risks, and take corrective action before small issues become costly problems.

Common Challenges in Project Accounting and How to Avoid Them

Managing project finances can quickly become complex due to unexpected changes, inaccurate data, and delayed reporting. Identifying these challenges early and addressing them proactively helps you maintain control and protect project profitability.

1. Uncontrolled Changes That Increase Project Costs

As projects progress, additional client requests, changing requirements, or unplanned tasks can increase costs and extend timelines, reducing overall project profitability if not properly managed.

How to Avoid it: Establish a formal change approval process before accepting new work. Update project budgets, timelines, and resource plans whenever project requirements change, and communicate those changes with all stakeholders.

2. Delays and Errors in Client Billing

Missing billable hours, inaccurate expense tracking, and manual invoicing can lead to delayed payments, billing disputes, and unreliable revenue tracking.

How to Avoid It: Record billable hours and project expenses in real time, automate invoice generation whenever possible, and review invoices carefully before sending them to clients.

3. Unrealistic Budgets and Cost Estimates

Estimating project costs without reliable data or accounting for hidden expenses often leads to inaccurate budgets and cost overruns.

How to Avoid It: Use data from previous projects to create realistic estimates, include contingency budgets for unexpected expenses, and review cost forecasts regularly throughout the project.

4. Limited Visibility into Project Finances

When financial data is scattered across multiple systems, it becomes difficult to track project performance and identify issues in time.

How to Avoid It: Use a centralized project accounting system that provides real-time visibility into project costs, revenue, budgets, and profitability, allowing you to make informed decisions as the project progresses.

How Does Time Champ Help Businesses Manage Project Accounting Effectively?

Keeping project finances accurate becomes difficult when billable hours, project costs, employee activities, and budgets are managed across multiple tools. Without real-time visibility, tracking profitability and controlling project expenses can become time-consuming. Time Champ is an employee monitoring software with built-in project management features that provides you with complete visibility into how time, resources, and project costs are utilized, helping to manage project accounting more efficiently.

Keyfeatures of Time Champ that support project accounting

- Automatic Time Tracking: Records work hours automatically and accurately tracks billable and non-billable time for every project without manual timesheets.

- Project and Task-Based Tracking: Monitors your time and effort spent on individual projects and tasks, making it easier to calculate project costs and evaluate profitability.

- Real-Time Productivity and Activity Monitoring: Provides visibility into employee productivity, application usage, idle time, and work patterns to optimize resource utilization and control labor costs.

- Comprehensive Reports and Analytics: Generates detailed reports on project hours, productivity, attendance, and resource utilization to support budgeting, financial analysis, and project performance reviews.

- Budget and Resource Management: Monitors project progress alongside resource allocation and work hours, helping you identify budget risks early and keep projects on track.

Conclusion

Managing project finances effectively requires accurate cost visibility, timely reporting, and informed decision-making throughout every stage of a project. A well-planned project accounting approach helps you control budgets, monitor profitability, improve resource utilization, and deliver projects with greater financial confidence. Following the proven processes, adopting the right accounting methods, and using tools that automate time tracking and project insights can reduce financial risks and improve overall project performance. Investing in the right system today lays the foundation for more profitable, predictable, and successful projects in the future.

Table of Content

What Is Project Accounting?

What Is Project Accounting?- Why Project Accounting is Important

- Project Accounting vs Financial Accounting: Key Differences

- How Does the Project Accounting Process Work

- What are the Most Common Project Accounting Methods

- Key Benefits of Project Accounting

- Common Challenges in Project Accounting and How to Avoid Them

- How Does Time Champ Help Businesses Manage Project Accounting Effectively?

- Conclusion

Related Blogs

See how employee monitoring strengthens accountability, improves transparency, and helps teams perform better without crossing into workplace surveillance.

Anjali | Jul 01, 2026

Familiarize yourself with the basics of Project Cost Management, including budgeting, and estimating the costs. Make sure that your projects are profitable.

Jahnavi Pulluri | May 21, 2024

Learn what a project description is, when and how to write one, pros and cons, and how it differs from a project proposal, with a ready-to-use template.

Guna Lakshmi | Apr 02, 2026Discover how employee productivity tracking builds accountability, drives ownership, and turns daily activity into measurable team performance.

Guna Lakshmi | May 01, 2026Improve project profitability with Time Tracking ROI by reducing wasted hours, controlling labor costs, increasing productivity, and boosting returns.

Anjali | Jun 03, 2026

Learn to create and leverage SMART goals effectively in project management for better planning, execution, and success. Get expert insights now!

Mounika Sai | Dec 06, 2023Ready to Manage Your Workforce Smarter?

Join our family of 1500+ companies using smart insights to redefine workforces!

Free Trial

No Credit Card Required